Budgeting •

November 2, 2022

Financial literacy for college students

Financial literacy involves learning basic money skills to manage your personal finances. Here’s everything college students need to know about money.

Managing personal finances is vital for a successful adult life—particularly these days when everything seems to cost an arm and a leg!

Despite the importance of money skills, they simply aren’t taught in schools. The responsibility to learn personal finance usually falls on the individual.

Why is financial literacy so important for college students? College is the time when you are laying a foundation for your future. If you set a good financial foundation now, you’ll be more likely to live a financially successful life.

This guide to financial literacy for college students covers just about everything you need to know about money skills while in college.

Components of financial literacy

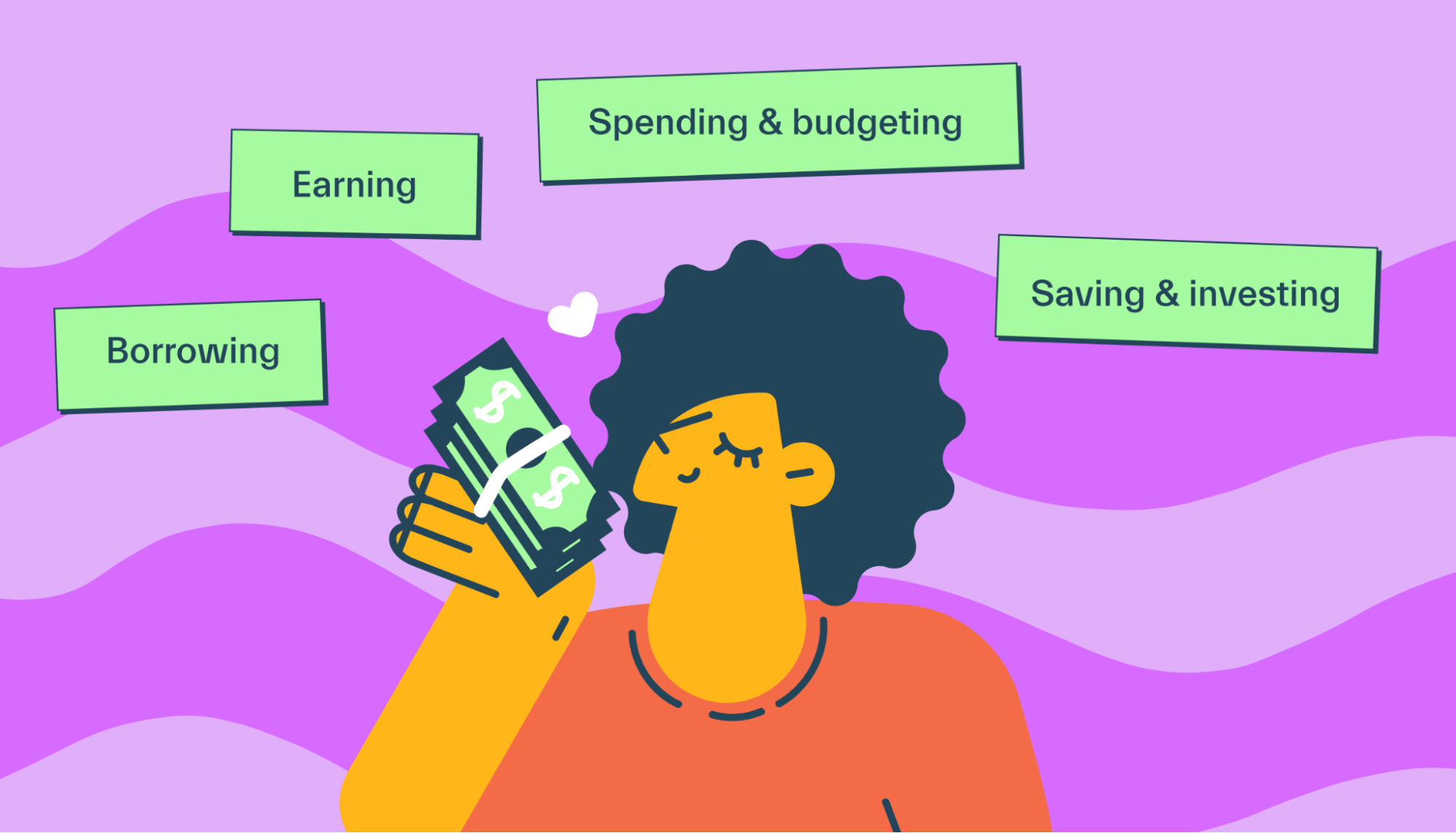

Financial literacy is a broad concept that covers all the basic principles of personal finance.

There are several broad components to be aware of.

Earning

Before you can save, invest, or really even plan, you must earn money. It seems obvious, but earning is the foundation of personal finance!

For students, earning may look a bit different from the general population. For many students, the primary source of “income” is financial aid or scholarships. Many students have part-time jobs or side hustles, but few work full-time.

To prepare your finances, it’s important to understand how much money you’re bringing in each month—both on a gross and net basis. “Gross” refers to total income, while net refers to income after taxes are taken out.

If you work a part-time job and earn $400 per week, your gross income is $1,600 per month—but your net income is likely a bit lower due to federal and state taxes being taken out of your paycheck.

If you have income from multiple sources (financial aid, work-study, etc.), then you’ll have to combine your income sources to figure out your total income. Once you have this figure, you can make a budget, work toward savings goals, and more.

Spending and budgeting

We all know how to spend money—but spending mindfully is another matter! For most students, money is tight, so it’s important to have a budget.

To start, you’ll need to calculate your net income (see above) and then tally up all your expenses. Start with the essentials—tuition, groceries, rent—before you budget anything for optional expense categories. We’ll discuss budgeting in greater detail below.

Borrowing

Getting a handle on debt involves understanding interest rates, credit scores, and the long-term impacts of borrowing.

Borrowing money is necessary for most students. Around 70% of students have student loan debt by the time they graduate, and many also take out other loans or accumulate credit card debt.

While borrowing is often a necessary component of student finances, it’s vital to understand the impact of debt. Debt can create a significant financial burden for years or even decades to come.

Student loans can seem abstract, as payments aren’t required until 6 months after graduation. But the burden of debt becomes very real very fast post-graduation.

Saving and investing

Any leftover funds can be used for saving or investing toward your financial goals.

The first step is to determine what your goals actually are!

Do you want to pay off your student loans early? Do you want to get a jumpstart on saving for retirement? Do you want to save up for a down payment or a new vehicle?

While in school, you might not have much extra cash to work with—but it’s still worthwhile to sit down and think about your financial goals in life.

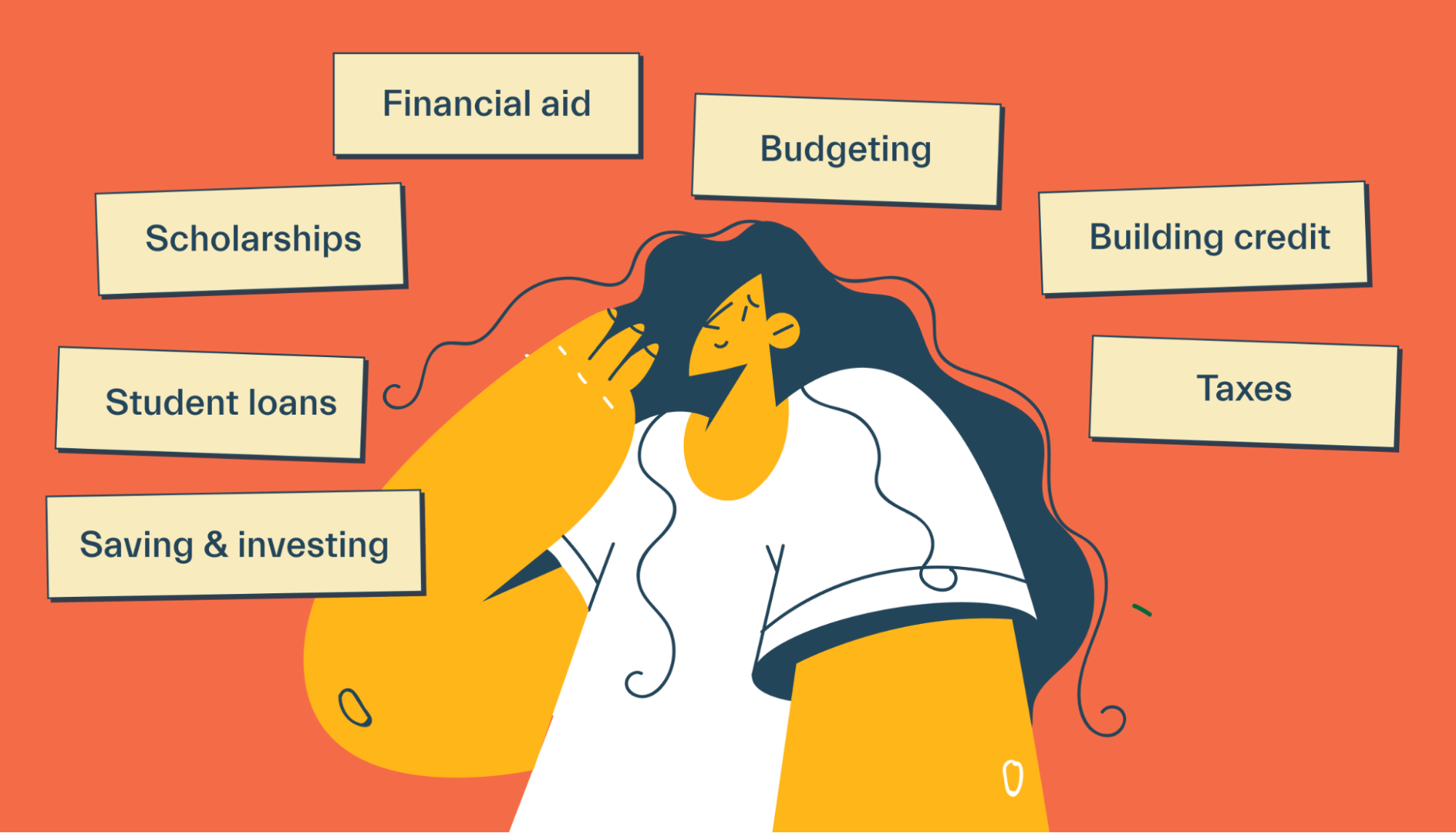

Financial literacy for college students

Financial literacy encompasses all aspects of personal finance. For students, the most important principles look a bit different than they would for the general population.

Here’s what students should focus on when learning financial skills.

Financial aid

Financial aid is all the money you can get from the government to help pay for college. It includes federal student loans, grants, scholarships, and work-study.

Financial aid is applied for using the Free Application for Federal Student Aid (FAFSA). This application is due every academic year. Filling out the FAFSA yearly is the most important thing students can do to improve their finances while in college. Completing the FAFSA determines how much financial aid you are eligible for.

“Financial aid” is a broad term, and there are several different types of financial aid to be aware of:

Scholarships: Scholarships are free money for college offered by the government, organizations, nonprofits, and companies. Scholarships do not need to be paid back. Most scholarships are applied for directly, outside of the FAFSA. However, completing the FAFSA is usually a pre-requisite to applying for scholarships.

Grants: Grants are free funds for college offered mostly by the government. They are often need-based, meaning that students from lower-income households will often qualify for more grants. Grants do not need to be paid back.

Work-study: Work-study is a program that allows students to work part-time jobs on campus or nearby. The program is a partnership between the government and private employers—students work for private employers (or the school itself), and the federal government helps cover some of the student’s wages.

Loans: Student loans are available to help cover the cost of attending college, but they must be paid back eventually—with interest. Fortunately, loan payments don’t begin until 6 months after graduation, so students will have some breathing room before it’s time to repay their loans.

It’s important to understand that most federal student aid goes directly to the school rather than the student. Financial aid will be applied to tuition and fees first. If there are funds left over, they may be transferred directly to the student to be used for living expenses.

Scholarships

Scholarships are available from a variety of sources, including private companies, nonprofits, governments, and colleges. They provide funds to students to pay for tuition or living expenses and do not need to be repaid.

Some scholarships are need-based (based on income), while others are available specifically for certain groups of people. For instance, there may be a scholarship for those pursuing engineering degrees or for first-generation college students.

It’s a great idea to apply for as many scholarships as you qualify for, as they can drastically reduce the cost of attending school. Here’s how to apply.

File the FAFSA. Most scholarships require that applicants have already filed the FAFSA for that academic year.

Search for scholarships. You can use BigFuture, Scholarships.com, Sallie Mae, or your school’s financial aid department. Look for scholarships that you qualify for (most list clear requirements for applicants). Mos can help you with applying for scholarships and grants while offering resources to improve your financial literacy.

Apply directly. Each scholarship will have its own application process. In general, students must submit a form and may be required to submit an essay or answers to writing prompts.

Keep applying. Don’t wait to hear back—keep applying for any scholarships that you qualify for. And remember, scholarships are based on academic years—so you can apply each year of college.

Student loans

Student loans are offered by the federal government, as well as private lenders. Most students take out federal student loans.

Federal student loans are applied for using the FAFSA. Once the application is processed, the government will calculate the maximum amount of federal loans that you can take out. From there, it’s up to you to determine how much you actually want to borrow.

Student loans must be paid back eventually, with interest. Students typically aren’t required to make payments until 6 months after graduation (or 6 months after dropping out). This is known as the student loan grace period.

Students should aim to exhaust all their other options before using student loans. In other words, you should aim to maximize your use of grants, scholarships, and your own savings before borrowing money for college.

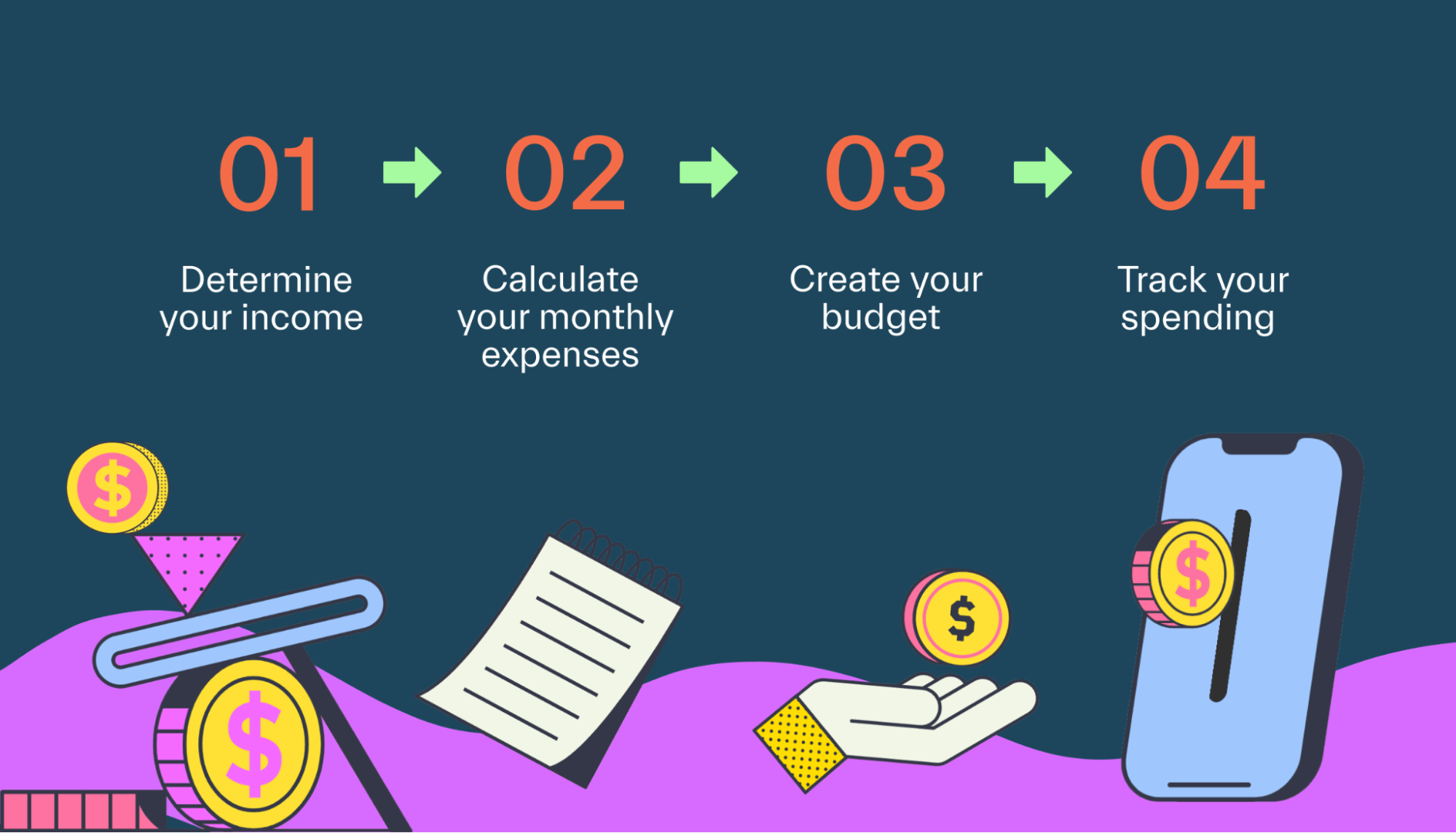

Budgeting

Budgeting is important for keeping your finances on track. This is particularly important for students, who often don’t have a whole lot of extra cash to work with!

To get started with budgeting, it’s helpful to use a budgeting app. These apps can help you track your spending, set goals, and track your progress.

If you’d rather go the manual route, you can use a college student budget template to get started.

The basic principle of budgeting is to first understand where your money is going every month and then make changes where appropriate to work toward your financial goals.

For instance, if you notice that you’re spending $200 a month on dining out, trimming that down a bit could allow you to allocate more towards student loan repayments. But until you start tracking your spending, you simply won’t know how much you’re spending on each category.

Building credit

Credit helps you apply for loans, credit cards, and even apartments. It’s measured using a credit score, which is a numerical score between 300 and 850.

Your credit score will be very important for the rest of your life. Generally speaking, the higher your credit, the easier it will be to get approved for loans—and the lower your interest rates will be.

Building credit in college could take a few different forms, including:

Opening a credit card and paying it off in full each month

Becoming an authorized user on a parent’s credit card

Beginning payments on your student loans to build a positive payment history

Making on-time payments on any loans you have

It takes time to build a positive credit history. The earlier you start, the more progress you can make by the time you graduate.

Taxes

Taxes are an unfortunate part of being an adult and are something that you’ll have to deal with for the rest of your life. Fortunately, college students often don’t owe much in taxes—but they will still need to file each year. Students may also qualify for certain college tax credits.

Many students don’t technically need to file a tax return as long as their income is under a certain limit. However, it’s still a good idea to file, as many students may actually get a tax refund when they file.

While manual filing is always an option, it’s much simpler to use software. Students can usually use free tax software to file simple tax returns. Free versions from TurboTax, Credit Karma Tax, and H&R Block will typically be sufficient for students.

The IRS also maintains a free resource of tax tips for college students.

If you live in a state with a personal income tax, you may also need to file state taxes.

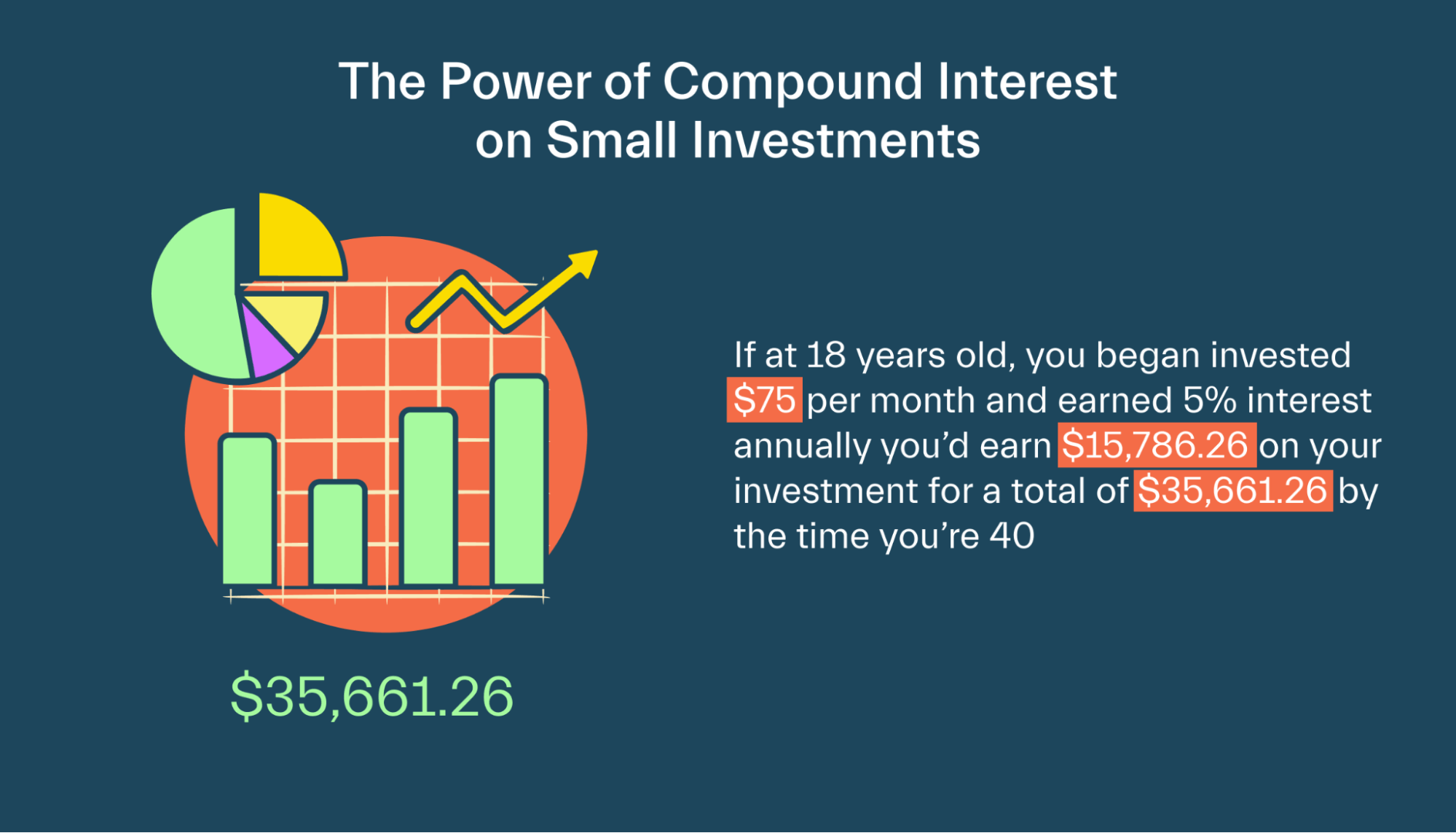

Saving and investing

If you find yourself with extra money in your budget, it’s wise to save it. Or, better yet, invest it for your future.

Even very small investments can grow substantially over long periods. Say you’re 20 years old and plan to retire at age 65. Consider these powerful examples:

Just $100 invested today will be worth around $2,100 after 45 years (assuming 7% average returns)

$100 per month will be worth a whopping $355,866 after 45 years

For many students, saving or investing can seem out of reach. But hopefully, these examples give you some perspective on the fact that it really doesn’t take much to make a meaningful difference in your financial future.

To learn more, read through our guide to investing for college students.

Financial resources for college students

Students are in a unique financial situation, but they also have unique resources available to them.

Here’s what to explore.

Mos

We believe all students deserve their dream degree without the debt. Mos helps students save on tuition, match with scholarships, and earn extra cash—all in one app.

Get an expert’s help with FAFSA, grants, scholarships, and more. Explore Mos memberships today.

College finance courses

If you’re interested in finance, you might consider enrolling in a finance-related course while in school. Even if you’re not pursuing a finance-related degree, some of these courses can be quite beneficial for any student.

It’s also worth looking into your school's community/continuing education classes. These classes are often offered in the evenings and teach a lot of real-life skills. If your school offers a personal finance continuing education course, it could be a great opportunity to learn valuable skills firsthand.

Campus financial aid department

Your school’s financial aid department is primarily there to help you with all things financial aid—but they’re also a great resource for finance in general.

If they can’t help you directly, chances are that they can point you in the direction of another resource that can.

Friends and family

Finally, don’t shy away from asking your friends and family for financial guidance. Parents, aunts and uncles, family friends, and older peers are all great resources. You may even have a friend your age who is interested in finance and could help answer any questions you have.

Wrapping up

Financial literacy is important for everyone, but it’s particularly important for young adults and students. With the tips and resources found above, you can be well on your way to a brighter financial future.

Let's get

your money

- Get paired with a financial aid expert

- Get more money for school

- Get more time to do you