Financial aid •

January 4, 2023

How to get a degree, debt-free

Graduating with little to no debt is tough these days. But it’s still possible, although with more work involved. Learn how to get a degree debt free.

You’ve probably heard about how back in the day, you could work during the summers and pay your way through college debt-free.

That’s not the case anymore, and that’s reflected in a startling number: the average student loan debt is now $37,693!

So, is it even possible to get a debt-free degree anymore? Or do you have to stick yourself with a luxury vehicle’s worth of debt for a good college education?

In this article, we’ll cover several ways you can strive toward a debt-free post-grad life—or, at least, one with limited debt.

The downsides of too much student debt

Student debt can make it harder for graduates to save money. Some of their salary goes toward that debt for years, putting them behind the saving and investing curve.

Meanwhile, other financial goals, like getting married or buying a home, may move further out of reach.

Higher interest rates—often found on private student loans—only worsen the problem since a large chunk of the payment doesn’t even reduce the loan balance.

Plus, you risk missing or being late on a payment. This can cost you more in late fees and hurt your credit.

Poor credit makes it harder to borrow and open new credit cards, leaving you further behind.

And all that’s only the financial cost—consider the stress of a loan payment hanging over your head every month for years or even decades.

Working hard before and during college can be stressful but could pay off financially and for your mental health. Here are several ways to do it.

1. Save for college beforehand

High schoolers usually don’t have many options for saving money that will completely cover college costs.

However, saving up as early as possible can make a big difference.

Even if you can only put aside enough for a semester of tuition, or even half the cost of tuition, that’s money you won’t have to borrow.

With that in mind, here are some ways to save up some cash in advance and cut college costs.

Work before college

A pre-college paycheck can go a long way. It feels great to earn your own money as a teen, and it’s tempting to spend it, but set aside at least some of it for college if possible.

After all, if you can set aside more cash now, you’ll have less debt later. You’ll essentially earn that money back after graduation in the form of lower loan payments.

With that in mind, high school students should open a bank account when they get a job. Then, they can set up direct deposit, so the money goes straight into their bank account, no questions asked. It makes saving easy.

Teenagers can’t open their bank accounts until they’re 18. But they can open a joint bank account with someone like Mos and have a parent sign on as a joint account holder.

The parent is a co-owner of the Mos account and can set certain spending limits to help their kid build good financial habits. In addition, Mos charges no fees, and account holders can earn reward points redeemable for cash by spending with their debit card.

When the teen turns 18, they can take their parent’s name off the account and use their saved earnings for college.

Also—the earlier you start working, the more work experience you have when you get to college. This may make it easier to land higher-paying gigs during college, which we’ll discuss later.

Do your best in high school

Strong grades and a well-rounded application expand your opportunities—and they can qualify you for more scholarship aid.

For one, you might qualify for a merit scholarship at your chosen school. And some schools automatically give you money for having a certain GPA and test scores.

Plus, you might be able to win scholarships like the National Merit Scholar program in high school, loading up your college funds even more in advance.

Open a college savings accounts

All 50 states and Washington D.C. offer 529 plans, which let you save for college with tax advantages.

Contributions aren’t deductible, but savings grow tax-free and can be taken out tax-free for qualified education expenses—tuition, fees, books, etc.

If your parents or other family members have already started one for you, that’s amazing! But, students can also start their own—if they’re already of legal age—or contribute some of their own cash to one set up by a family member.

Take prior learning assessments

Prior learning assessments (PLAs) may help you earn college credit beforehand for much less than the credit hours will cost.

Advanced Placement (AP) courses are one of the most well-known PLAs. These let you take college-level courses in high school and gain credit for entry-level courses at colleges and universities if you get a high enough score on the AP test.

Take enough AP classes, and you could potentially test out of an entire semester’s worth of classes. That said, credit eligibility depends on your school and AP test scores.

There are numerous other PLA programs, including:

International Baccalaureate (IB)

College Level Examination Program (CLEP) exams

DSST exams

Portfolio-based assessments

Consider dual enrollment

Dual enrollment lets you take actual college courses during high school—usually at a local community college—for college credit.

These can help you save thousands of dollars on your college degree because you’ll generally have to pay far less for these courses than regular tuition.

Dual enrollment and PLAs together also help you graduate in less time once you reach college.

That means you can find a job and start earning a salary earlier, positioning yourself for more financial success.

2. Pick an affordable school

A lot goes into picking a school, from majors offered to campus life to the surrounding community (such as urban vs. rural).

Your budget should be in there as well. If graduating debt-free is a priority, the cost of attendance is an important factor to consider.

Here are some options for limiting your college costs and keeping debt low.

In-state vs. out-of-state vs. private tuition

At public universities, in-state tuition is generally much cheaper than out-of-state. Therefore, if you want to go to a state school, staying in your home state is often a financially wise choice.

That said, some public universities have eliminated out-of-state tuition to make themselves more accessible.

Then, there are private colleges and universities. These are usually far more expensive than public schools—but sometimes only on the surface.

Many offer more aid to offset the higher costs, potentially making these as affordable as public schools! Don’t rule out private institutions just because of the price tag.

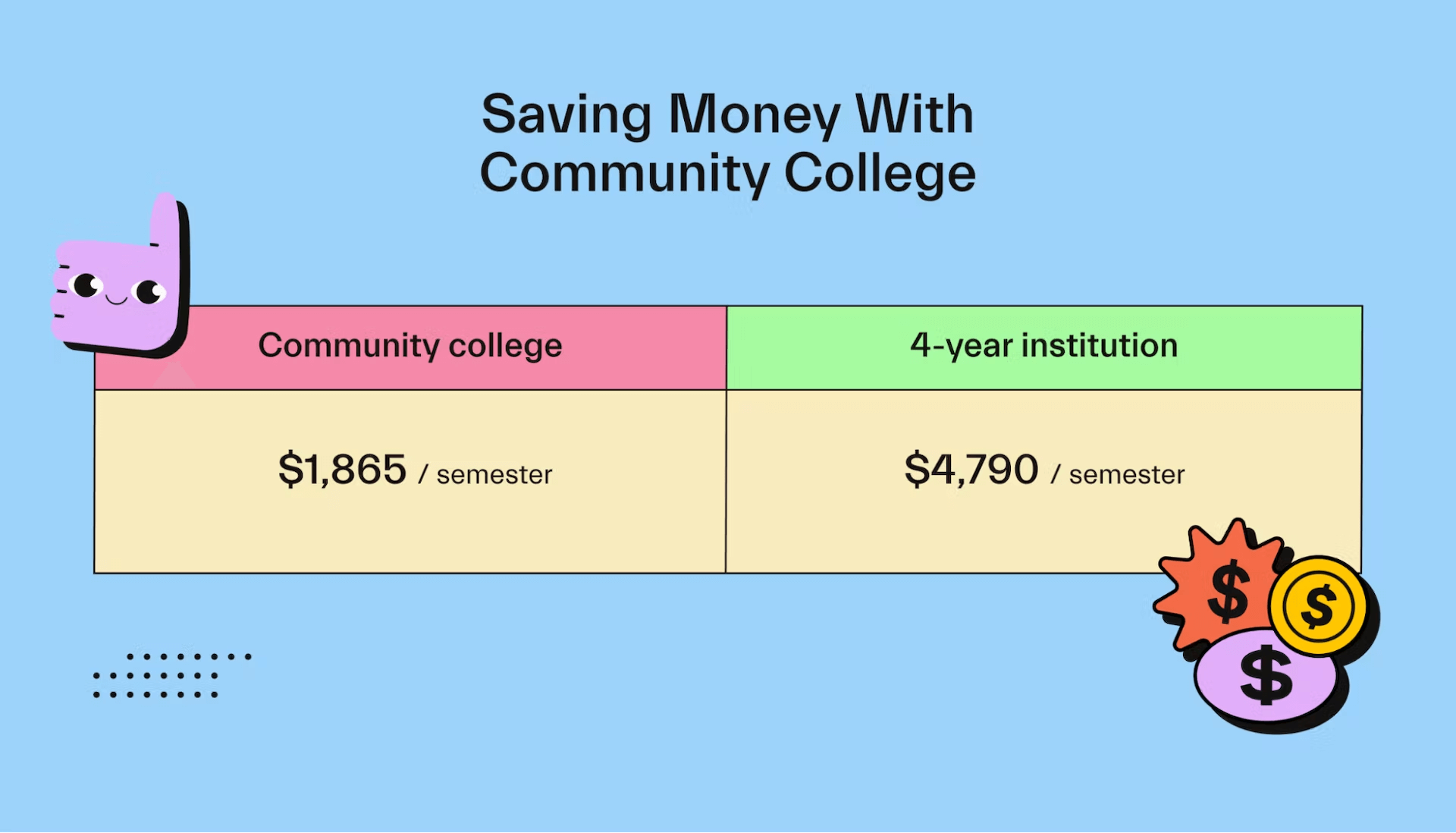

Going to community college first

Community colleges can offer similar academic rigor for much less money, and credits earned in community college are almost always transferable to most schools, meaning you can take most general education classes at a huge discount.

The average community college tuition is about $1,865/semester or about $467/month. Compare that to an average in-state tuition of $4,790/semester at 4-year institutions.

You might be able to cover most or all of that with a part-time job—depending on your pay—helping you avoid a lot of debt.

Plus, if you live at home, you can save on housing costs.

Attending college online

The internet is amazing—you can earn a 4-year bachelor’s degree entirely from your computer through online degree programs.

And it’s a lot cheaper—an online degree costs nearly $11,000 less on average than an in-person degree!

However, you aren’t limited to online-only universities. Many brick-and-mortar institutions have fully online degree programs, delivering high-quality education for less.

Consider some other financial benefits of online school:

More flexibility in your living situation could help you save on housing costs.

Time savings allow you to work more without sacrificing academics, helping you graduate debt-free.

Plus, many online programs are accredited nowadays, meaning they can take Free Application for Federal Student Aid (FAFSA). Check out our list of the top online colleges that accept FAFSA for more information.

3. Explore your financial aid options

The main thing you should do in terms of seeking financial aid is to fill out your FAFSA every year.

This helps determine your eligibility for loans, as well as grants and scholarships (which you don’t have to pay back).

Let’s look at some of the non-debt types of aid you might find.

Scholarships

We touched on scholarships already. A scholarship is money you can win for all sorts of reasons—and you usually don’t have to pay them back.

Most schools have a few merit-based scholarships, but you can also find thousands of others through state and local governments and private organizations.

Mos, by the way, can make that scholarship search easy.

Start by taking a quiz to match with tons of scholarships you could qualify for. Want some help applying? Work with a personal advisor to maximize your chances of winning and answer other financial aid questions you have--all in your app.

Grants

Grants are typically need-based forms of financial aid that you don’t have to pay back. The federal Pell Grant is the most well-known, but a few other federal programs are available.

States may offer state-based grants as well. However, many require you to complete the FAFSA to apply for their grants.

For example, New York helps eligible New York resident students pay for college through the New York State Tuition Assistance Program. Students must file the FAFSA to qualify to apply for the NYS TAP program.

You can also often find grants through private organizations; some aren’t just limited to those in need.

Work-study

Work-study is a federal financial aid program that lets you “pay” for school by working at approved o n-campus or off-campus jobs.

In general, your job will be somehow related to your major or field of study. Otherwise, it’ll usually be tied to civic education, such as a job at a government agency.

Work-study sometimes pays less than a part-time job outside the work-study system. However, work-study jobs generally have fewer hours and are more lenient about scheduling your classes around your job.

Military service

Serving in the military can qualify you for the GI Bill once you’re out (as long as you’re not dishonorably discharged). The GI Bill covers a large amount of your tuition and provides allowance and stipends for housing and books.

Beyond that, many military veteran-related organizations offer scholarships, grants, and other forms of aid to families of current and former service members and veterans.

Job tuition reimbursement

Today, more companies are offering tuition reimbursement to attract educated talent.

This isn’t just for full-time, post-college jobs, either. Companies that are offering this benefit to a wide range of employees include:

AT&T

Bank of America

Chipotle

Home Depot

Starbucks

UPS

Walmart

Alongside a paycheck, tuition reimbursement directly cuts your tuition costs and reduces your need for debt.

4. Find ways to save during college

Once you’re in school, you can still take a few steps to save money here and there on college expenses. Every dollar goes a long way toward graduating debt-free.

Here are some ideas for saving and earning a little extra.

Get a resident advisor job

Resident advisor (RA) positions are student jobs that involve planning activities for and generally managing on-campus dorms. You’ll ensure that students aren’t breaking any rules and plan dorm activities that facilitate socialization and fun.

Residence advisors generally have their meals and housing paid for by the school. Of course, you’ll still pay tuition, but having these essentials covered helps you stay debt-free.

Plus, living on campus might mean you’re close to the lecture halls. So you might be able to ditch the car or at least cut down on commuting costs for in-person classes.

Work part-time

If you have the time after knocking out homework and studying, pick up some part-time work.

Bonus points if it’s in your field of study—it could pay off later in your job search.

Paid internships often pay pretty well, especially in certain majors. These can make a huge financial difference, especially if it’s a full-time summer internship.

Beyond that, consider the non-wage perks of certain jobs.

For example, working for campus dining might earn you extra free meals. Plus, being on campus places you close to classes—no need to budget as much time for travel each day.

Meanwhile, working at a bookstore might get you discounts on books. Yep, you could get those expensive books for a little bit less!

Do gig work

Gig work is not the same as a job—it’s more of a “freelance” arrangement. For example, driving for Uber or delivering for Doordash are considered gig work.

These jobs require a bit more work, but they’re often easy to build around your class schedule.

The gig marketplace at Mos compiles tons of gigs suited specifically for the busy college student. Selling your class notes, walking your neighbor’s dog, tutoring fellow students…these are just a few fun gigs you’ll find in the gig marketplace at Mos.

Do a few of these, earn points, and redeem those points for cash. It’s that easy.

Apply for scholarships wherever possible

Scholarship opportunities don’t end when you enroll in classes.

There are plenty of scholarships available—some through your school, but many more outside of it. They can be based on your major, school, background, and more.

Set aside some time every week, such as during the day or weekend, and hunt for these scholarships. Every free dollar counts.

Once again, if you open a Mos account, your Mos advisor will help throughout your academic career. Feel free to lean on them to find scholarships year-round.

Rent (don’t buy) textbooks

If you buy textbooks, you can sell them later, but you won’t get back much money in many cases.

Today, plenty of textbook companies let you rent your textbooks instead for just a few bucks. You could save money here if you keep them in good condition and send them back on time.

That said, do the math of buying and selling vs. renting first. In some cases, buying could be the better option—especially if you buy used textbooks.

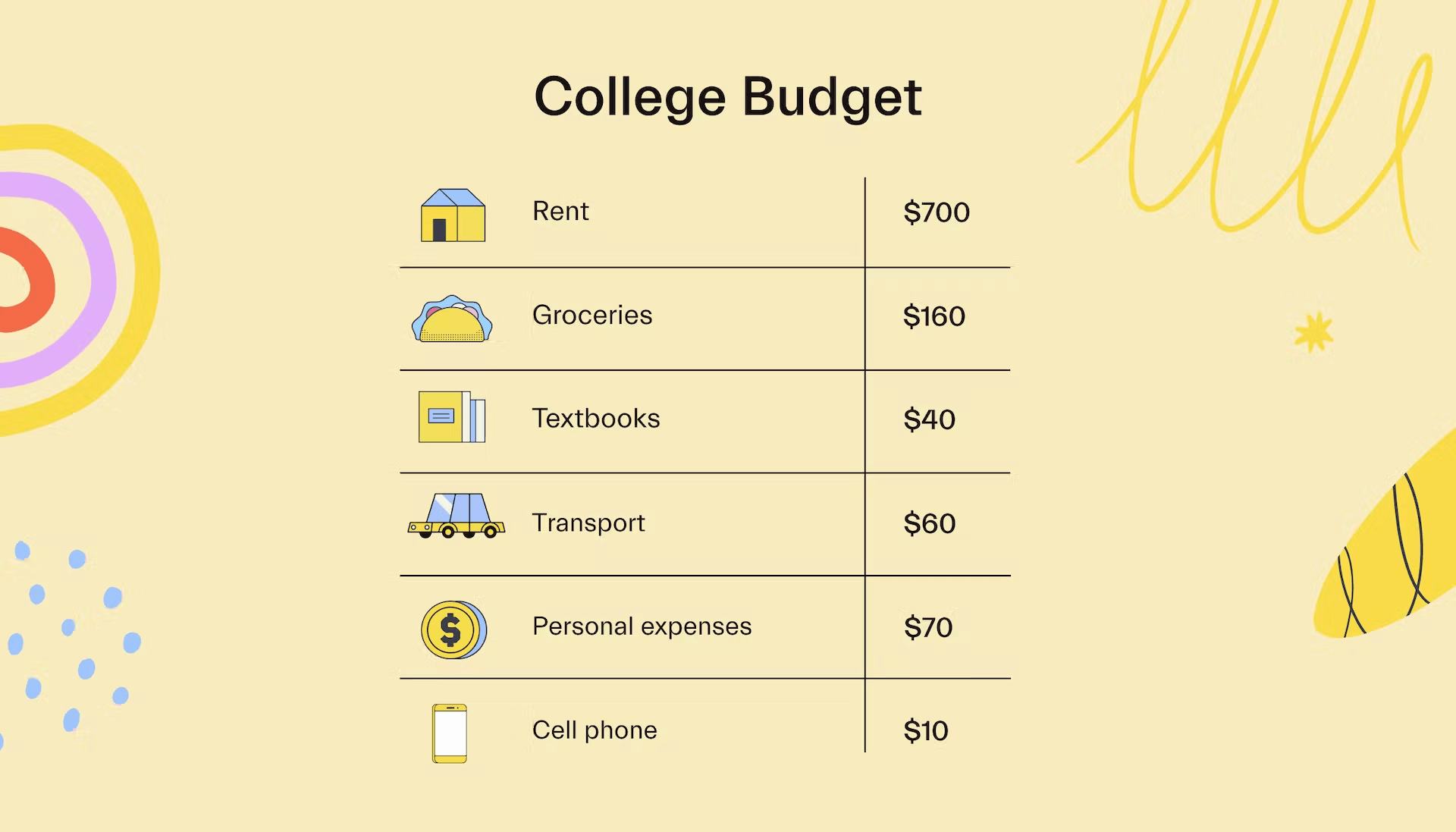

Create (and stick to) a budget

Running out of money and going into credit card debt is all too common among students who have little money in the first place.

Creating and sticking with a budget helps you avoid this for 2 reasons:

Expense cutting: You might spend on things you don’t use or can cut back on without much trouble.

Expense tracking: You see how much you’re spending every month vs. how much you make, and you can ensure new expenses don’t creep in.

Budgeting can be hard when you’re a broke college student, but we created a quick guide about how to create a student budget to help you out.

Get your degree and ditch the debt

Graduating college debt-free may seem impossible. And there’s some truth to that—it’s not easy, especially now.

But you still have tons of ways before and during your higher education experience to whittle away at the total cost of college and graduate with, at the very least, a manageable debt load.

Check out our other articles to learn more about affording college and reducing student debt.

Let's get

your money

- Get paired with a financial aid expert

- Get more money for school

- Get more time to do you